- Trending

- Comments

- Latest

Circle, issuer of the USDC stablecoin, is weighing the introduction of reversible stablecoin transactions, a move that could alter one of the founding principles of blockchain technology: the immutability of payments.

Speaking to the Financial Times, Circle president Heath Tarbert confirmed the firm is researching mechanisms that would allow transactions to be rolled back in cases of fraud or hacks.

“We are thinking through whether or not there’s the possibility of reversibility of transactions, right, but at the same time, we want settlement finality,” Tarbert said. “So there’s an inherent tension there between being able to transfer something immediately, but having it be irrevocable.”

For years, the crypto ethos has rested on the principle that once recorded on-chain, transactions are permanent. The exploration of reversible stablecoin transactions highlights the growing clash between decentralization ideals and the demands of institutional adoption.

Supporters argue that reversible stablecoin transactions could strengthen consumer protection, especially for victims of scams. In an industry where fraud losses are estimated to exceed billions annually, the ability to recover stolen assets may boost mainstream trust.

But critics warn the concept undermines one of crypto’s core features: immunity from centralized control. “Immutability has always been crypto’s greatest guarantee once we compromise that, we risk turning blockchains into just another bank ledger,” said Andrei Grachev, founding partner at liquidity protocol Falcon Finance, in a comment.

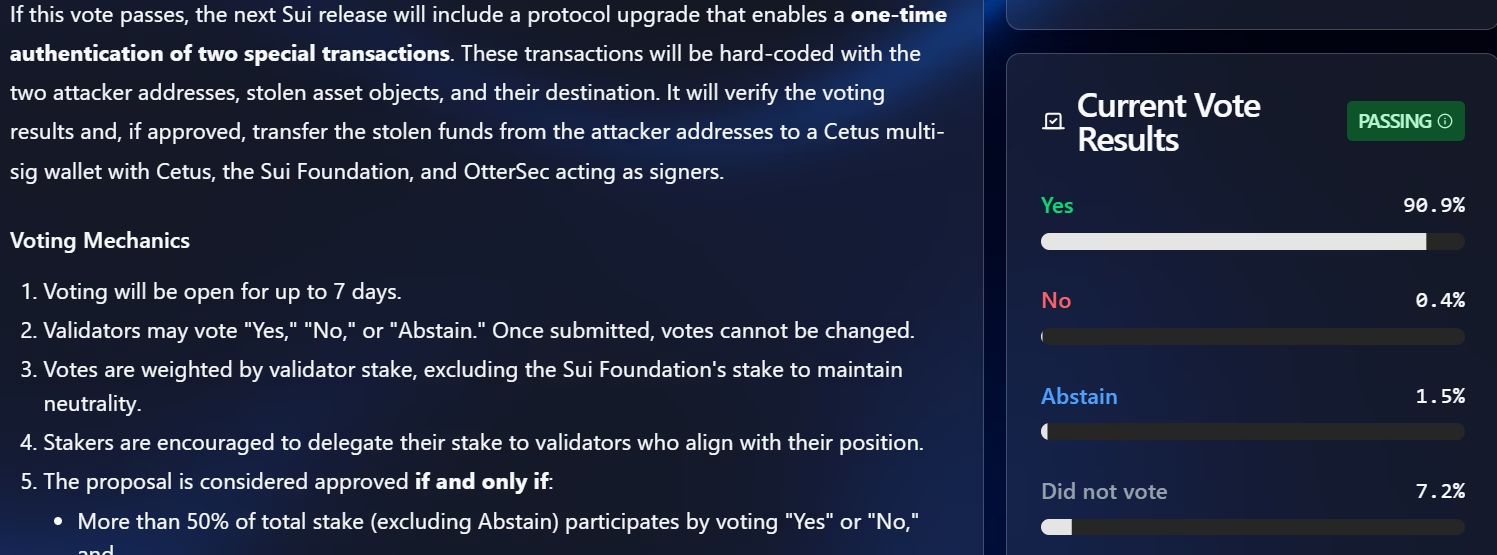

The debate isn’t purely theoretical. In May, decentralized exchange Cetus was exploited for more than $220 million in assets. Validators managed to freeze $162 million, later returning funds to the platform. The incident showcased the potential benefits of reversibility while also fueling concerns that validators now wield power to intervene in ways previously thought impossible.

Tarbert suggested that elements of traditional finance (TradFi) could inspire solutions for blockchain’s next phase.

“People say blockchain technology, stablecoins, smart contracts, are superior in technology to the current system. But there are some benefits of the current system that aren’t necessarily currently present,” he said.

In TradFi, chargebacks and fraud protections are standard. Circle’s experiment with reversible stablecoin transactions would effectively bring similar safeguards into the digital asset ecosystem. Proposals could include smart contracts with refund triggers or permission-based stablecoins that allow temporary settlement delays in suspected fraud cases.

This approach is not without precedent. Payment systems worldwide rely on reversibility to mitigate fraud risks, and regulators may view such mechanisms as essential before stablecoins gain full acceptance. “In that context, reversibility is not a flaw,” Grachev said. “Instead, it can be a functional feature when designed with clear rules, user consent and onchain enforcement.”

Circle’s exploration of reversible stablecoin transactions comes amid a broader strategy to deepen its institutional footprint. In August, the company unveiled Arc, its new layer-1 blockchain designed for enterprise-grade stablecoin payments, foreign exchange, and capital markets. Arc will use USDC as its native gas token, with a public testnet planned this fall and a full launch by the end of 2025.

The rollout will integrate with Fireblocks, a digital asset custody and tokenization provider used by over 2,400 banks. This means Circle’s institutional partners from banks to asset managers will have direct access to blockchain payments from day one.

By combining its infrastructure expansion with potential safeguards like reversible stablecoin transactions, Circle is signaling to policymakers and enterprises that it intends to bridge the gap between crypto innovation and traditional financial standards.

The introduction of reversible stablecoin transactions would likely require clear governance frameworks to avoid abuse. Questions remain: Who decides which transactions can be reversed? What criteria define fraud? And how can trust be maintained if reversibility introduces subjective decision-making?

Reports shows that Circle has not yet provided details on implementation, but industry observers believe a consent-based system could be key. For instance, users might opt into reversible settlement channels for higher security, while advanced users could stick with immutable transfers.

Still, the move could have far-reaching implications. Regulators may see reversible stablecoin transactions as a positive development, bolstering consumer protection. But decentralization advocates worry that the shift could set a precedent where corporate or governmental powers can influence blockchain transactions.

For now, Circle’s idea remains under examination, but the debate underscores the industry’s broader evolution: from crypto’s radical independence to a more regulated, institution-friendly model. Whether reversible stablecoin transactions become the norm or remain an experiment will depend on how the crypto community, regulators, and financial institutions respond in the months ahead.

Copyright © 2025 - The Bit Gazette.

{kind=link}