- Trending

- Comments

- Latest

Standard Chartered Bank has projected that over $1 trillion in deposits could exit emerging market banks and move into stablecoins by 2028, driven by inflation, currency instability, and growing access to U.S. dollar-pegged digital assets.

According to a Global Research report released Monday, stablecoin holdings for savings in emerging markets could surge from $173 billion currently to $1.22 trillion within three years—a sevenfold increase that would represent one of the largest capital shifts in modern banking history.

‘Stablecoin ownership has been more prevalent in emerging markets than in developed ones,’ the report states. ‘This suggests that diversification toward stablecoins is likely to accelerate, especially in high-inflation regions.’

The projection comes as countries including Venezuela, Argentina, and Brazil see rapidly accelerating stablecoin adoption, with users increasingly treating USDT and USDC as safer alternatives to local currency bank deposits.

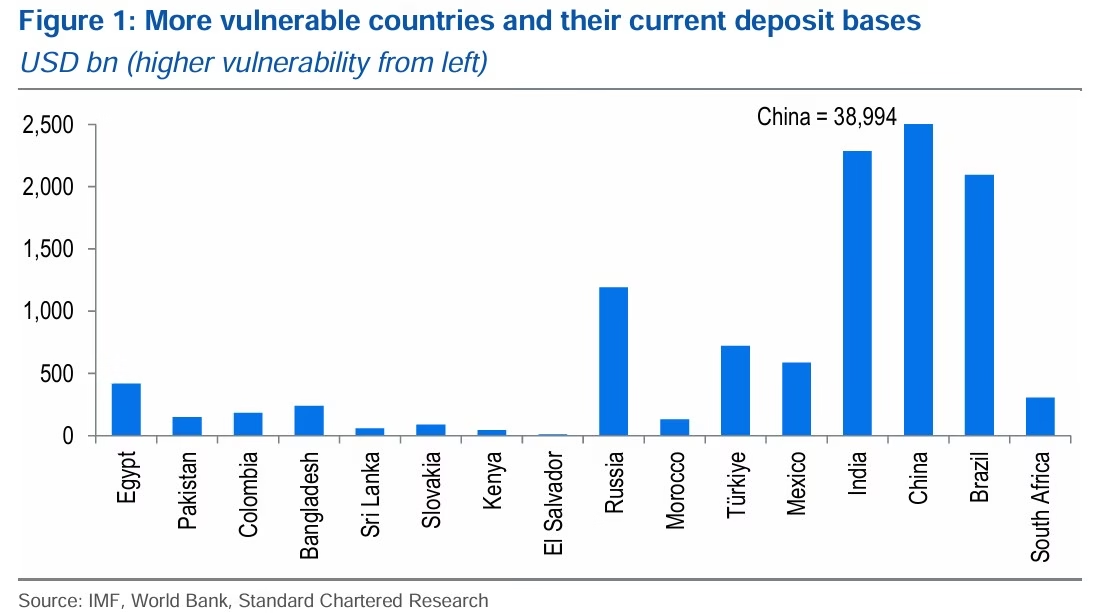

The report emphasizes that the Standard Chartered stablecoin outflow will hit hardest in emerging markets (EMs), where banking systems are already strained by inflation and capital flight. These regions including Latin America, Africa, and parts of Asia are experiencing growing adoption of digital assets as a hedge against local currency instability.

According to the report, roughly two-thirds of all stablecoin supply is already concentrated in emerging markets. Users are increasingly turning to digital wallets as substitutes for dollar-denominated bank accounts, benefiting from 24/7 liquidity and reduced exposure to local credit risk.

Stablecoins are seen as safer alternatives to deposits held in domestic banks, as the U.S. GENIUS Act requires stablecoin issuers to maintain full dollar reserves. Standard Chartered cautioned that this structural difference could accelerate the Standard Chartered stablecoin outflow, draining deposits from EM financial institutions.

The key risk is that domestic banks may lose their deposit base faster than they can adapt, the report stated. As customers migrate to stablecoins, credit availability and local lending capacity could be severely constrained.

Economist Dr. Maria Adewale from the African Institute of Digital Finance said the trend reflects a “trust gap” in local banking systems. “The Standard Chartered stablecoin outflow shows how emerging markets are leapfrogging traditional finance infrastructure but it also poses a threat to financial stability if left unmanaged,” she told CryptoBrief.

Countries like Venezuela, Argentina, and Brazil are leading this movement toward stablecoin reliance. In Venezuela, where inflation has hovered between 200% and 300%, stablecoins such as USDT colloquially known as “Binance dollars” have effectively replaced the bolivar as a unit of account.

According to a Chainalysis 2024 report, Venezuela ranked 13th globally for crypto adoption, with a 110% increase in stablecoin usage over the past year. Small merchants, grocery chains, and entertainment venues now regularly accept stablecoin payments via Binance and Airtm.

In 2023, crypto accounted for roughly 9% of Venezuela’s $5.4 billion in remittances, according to data from the Inter-American Development Bank. That figure is projected to exceed 15% in 2025, as traditional remittance services like Western Union have reduced operations due to sanctions and currency restrictions.

Argentina’s peso has depreciated over 90% against the dollar since 2023, despite President Javier Milei’s economic reforms. Stablecoin usage has surged as citizens seek to preserve purchasing power, with peer-to-peer USDT trading volume on Argentine exchanges exceeding $2 billion monthly, according to LocalBitcoins data.

Argentine retailers, particularly in Buenos Aires, increasingly price goods in USDT to avoid daily repricing due to inflation, which exceeded 140% annually in 2024.

While Brazil’s inflation is more moderate (4-6% annually), strict capital controls limiting foreign currency purchases to $10,000 per year have driven adoption of stablecoins for international transactions. Brazil’s Central Bank estimates that $8-12 billion in stablecoin transactions occur monthly, though the figure is difficult to verify due to the decentralized nature of blockchain networks.

A recent report by Fireblocks found that stablecoins now make up 60% of all crypto transactions in both countries. This reinforces Standard Chartered’s assertion that stablecoins have evolved from speculative instruments to essential tools for financial stability in unstable economies.

“The data validates our view that the Standard Chartered stablecoin outflow is part of a broader structural transformation,” said Alex Manson, Head of Ventures at Standard Chartered. “For millions of users, stablecoins are becoming their first and most trusted entry point into digital finance.”

Standard Chartered’s 2028 projection will face its first major test in 2026, when several emerging market economies including Argentina, Turkey, and Nigeria hold presidential elections that could reshape crypto policy.

The bank recommends that emerging market central banks develop ‘stablecoin-compatible regulatory frameworks’ that integrate dollar-pegged digital assets into supervised financial systems rather than pushing them into unregulated channels.

For traditional banks, the message is stark: adapt by offering stablecoin custody, remittance, and payment services, or risk losing deposits to purely digital competitors that can serve customers 24/7 without brick-and-mortar overhead.

Whether the $1 trillion outflow materializes will depend on three factors: inflation trajectories in major emerging markets, regulatory responses from governments, and the willingness of traditional banks to integrate rather than resist the stablecoin economy.

Copyright © 2025 - The Bit Gazette.

{kind=link}