- Trending

- Comments

- Latest

The Federal Government of Nigeria has taken a major step toward Nigeria stablecoin adoption, establishing a dedicated working group to explore how digital currencies can be integrated into the nation’s financial system.

The initiative, announced by Central Bank of Nigeria (CBN) Governor Olayemi Cardoso, represents one of the most progressive policy pivots on digital assets in the country’s history.

The announcement came during a joint press briefing in Washington, D.C., following the annual meetings of the World Bank and the International Monetary Fund (IMF).

According to Cardoso, the Central Bank, in collaboration with the Ministry of Finance and other key institutions, has formed teams to assess the regulatory, economic, and technological implications of Nigeria stablecoin adoption.

“The message from there is that the Central Bank Governor, the Ministry of Finance, and others reached a general consensus on the need to support innovation and ensure it continues,” Olayemi Cardoso, Governor, Central Bank of Nigeria, said during the briefing. “By no means does anybody want to stifle innovation. However, there is also a need to balance this with the risks involved in these new technologies and digital currencies.”

This announcement underscores Nigeria’s evolving attitude toward digital assets, contrasting sharply with the restrictive policies seen under the Muhammadu Buhari administration.

The formation of this task force signals a broader governmental recognition of the potential benefits of Nigeria stablecoin adoption, both for enhancing financial inclusion and modernizing the economy.

Stablecoins as cryptocurrencies pegged to traditional fiat currencies have become key instruments for cross-border transactions, remittances, and liquidity management in emerging markets.

Under President Bola Ahmed Tinubu’s administration, Nigeria has been pursuing a more innovation-driven approach to the financial sector. Recent initiatives include granting operational licenses to at least two digital asset exchanges and enacting legislation to establish a legal framework for the digital asset ecosystem.

According to Cardoso, the Nigeria stablecoin adoption effort is part of a larger strategy to align monetary policy with innovation while ensuring systemic safety.

“We have made it clear that the Central Bank is not against technological advancement. What we seek is responsible innovation that complements our economic goals,” — Cardoso emphasized during the press conference.

In parallel, the government has also announced plans to begin taxing cryptocurrency gains from 2026 which is a move intended to bring regulatory clarity and mainstream recognition to digital asset trading within Nigeria.

Cardoso noted that the Nigeria stablecoin adoption framework will involve close consultation with stakeholders across the financial, technology, and legal sectors.

The working group aims to examine issues such as consumer protection, anti-money laundering (AML) compliance, and the potential role of stablecoins in cross-border payment systems.

The balance between innovation and regulation is delicate, Aisha Abdullahi, fintech policy analyst at the Nigerian Economic Summit Group (NESG), said in an interview.

Nigeria’s proactive move on stablecoins demonstrates maturity in its financial policy thinking. It’s a signal that the country wants to participate actively in shaping global crypto standards rather than reacting to them.

Stablecoins have attracted attention globally for their potential to simplify transactions and reduce costs, especially in countries with volatile currencies.

For Nigeria where the naira has faced sustained devaluation, Nigeria stablecoin adoption could present a pathway to improving access to more stable, digital payment alternatives.

The CBN’s evolving stance reflects lessons learned from its earlier restrictive approach to crypto transactions. In 2021, the bank prohibited financial institutions from facilitating crypto-related transactions, a move that drove digital trading underground and limited oversight.

Since then, policymakers have acknowledged that regulation, not prohibition, offers a more sustainable path forward.

According to the News, the government’s new framework aims to integrate cryptocurrencies, stablecoins, and tokenized assets into formal economic systems, strengthening transparency and taxation mechanisms.

The Nigeria stablecoin adoption initiative, therefore, stands as a strategic pivot to legitimize and supervise the fast-growing crypto economy.

Cardoso confirmed that this initiative will include continuous dialogue with Nigeria’s fintech ecosystem, citing a recent strategic session between the CBN and fintech leaders.

“Our commitment to collaboration remains firm,” he said. “Nigeria’s future lies in open dialogue between regulators, innovators, and the public.”

Nigeria’s decision to formalize its stablecoin adoption strategy comes as other emerging economies including Brazil, Singapore, and the UAE explore integrating blockchain-based payment systems into their national frameworks.

For Nigeria, the largest economy in Africa, this move positions it as a regional leader in regulated digital currency development.

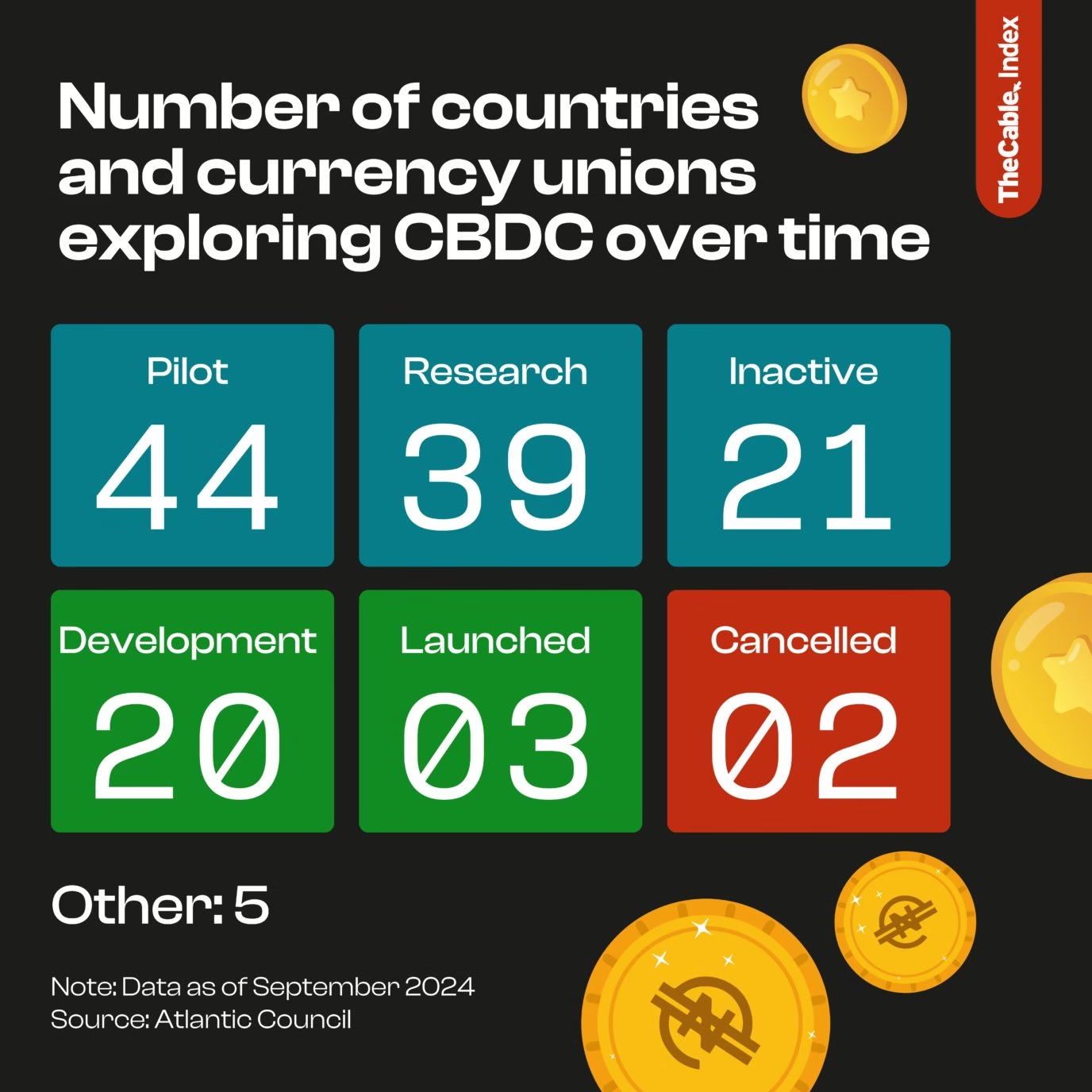

Experts believe the Nigeria stablecoin adoption roadmap could also complement the country’s eNaira, a central bank digital currency (CBDC) launched in 2021.

While no timeline has been provided for the rollout, analysts anticipate that pilot programs and stakeholder consultations could begin before mid-2026.

Copyright © 2025 - The Bit Gazette.

{kind=link}