- Trending

- Comments

- Latest

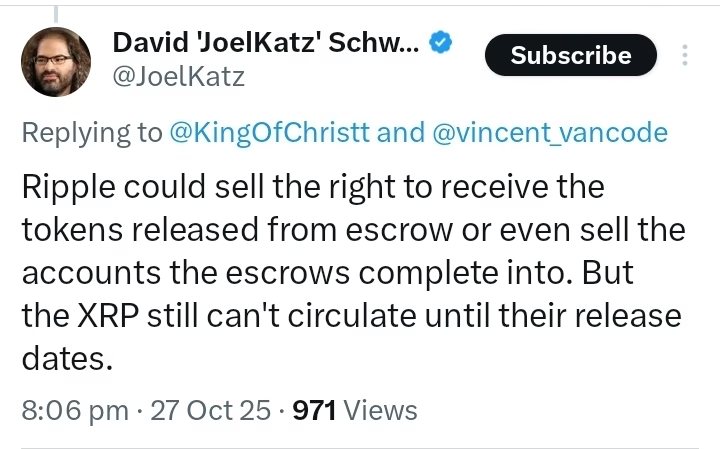

Ripple’s Chief Technology Officer, David Schwartz, has disclosed a striking detail about the company’s XRP escrow fact, sparking fresh discussions among crypto investors about how XRP’s supply should be interpreted.

Responding to ongoing debates on X (formerly Twitter), Schwartz confirmed that although the XRP locked in Ripple’s escrow accounts cannot enter circulation until their scheduled release dates, Ripple can sell or transfer the rights to receive those tokens in advance.

In his post on October 27, 2025, Schwartz wrote:

The revelation introduces an important nuance to the long-standing conversation around Ripple’s locked holdings, and adds a layer of complexity to how total and circulating supplies are understood within the XRP ecosystem. For investors tracking XRP escrow fact and its effects on market perception, Schwartz’s comment offers fresh perspective on Ripple’s financial flexibility.

Ripple’s XRP escrow fact centers on the 35 billion XRP currently held in thousands of time-locked contracts. These escrows were designed to release a fixed amount of XRP each month, preventing sudden market oversupply. Data from the XRP Ledger shows that 14,180 separate escrow accounts currently hold 35,046,399,781 XRP, representing about 30 percent of the total token supply.

Until now, those holdings were largely considered inaccessible until each scheduled release date. Schwartz’s clarification suggests otherwise: while the XRP itself cannot move early, the legal rights to receive future releases can be transferred, sold, or monetized.

This means Ripple could, in theory, use the future value of locked XRP as a financial instrument — possibly to secure credit lines, back investments, or structure strategic partnerships — without breaching the network’s technical restrictions. However, it does not increase liquidity or accelerate token release.

The XRP escrow fact also impacts how the token’s market capitalization is calculated. Bitcoin’s market cap includes every coin ever mined — even those that are lost or inactive. XRP, by contrast, excludes tokens locked in escrow from its circulating supply count.

This difference has long been a source of contention among analysts who argue that XRP’s ranking and market influence appear understated. The ability to transfer rights to escrowed tokens blurs the line between “locked” and “available,” raising questions about how such assets should be reflected in financial metrics.

Schwartz’s statement effectively reframes the escrow system as not only a technical safeguard but also a transferable asset class — an approach that could influence both institutional valuation models and investor sentiment toward XRP.

For investors, the XRP escrow fact highlights how Ripple’s asset management practices could influence long-term supply transparency. The clarification does not signal any immediate change to circulating supply, the tokens remain time-locked — but it underscores Ripple’s capacity to leverage escrowed assets without altering on-chain liquidity.

As speculation grows around the potential approval of an XRP exchange-traded fund (ETF), this new information could become relevant for how regulators and issuers interpret the asset’s underlying reserves. Analysts suggest that future financial disclosures from Ripple might need to differentiate between “escrowed XRP” and “escrow rights sold or pledged.”

In a market where clarity and credibility shape investment flows, the XRP escrow fact reopens vital questions about supply definition, valuation fairness, and the intersection of legal ownership with blockchain constraints.

Copyright © 2025 - The Bit Gazette.

{kind=link}