- Trending

- Comments

- Latest

Tokenized U.S. Treasuries now yield 5% on-chain, escalating the TradFi vs DeFi showdown. Over the past years, real-world asset (RWA) tokenization has exploded like popcorn in a microwave as institutions hunt for safer, yield-generating crypto products.

For example, BlackRock’s shiny new “BUIDL” tokenized money-market fund is a typical case, amassing over $2.8 billion in on-chain Treasuries within months.

All said, demand for tokenized bonds has smashed records like a wrecking ball through a glasshouse. So today, we’re diving into the forces driving this 5% yield story, unpacking the risks that could change everything, in the TradFi vs DeFi conversation, the blockchain welcoming them and powering the deals.

At its core, tokenization is simply putting real assets on the blockchain i.e real assets like bonds, mortgages, or even real estate deeds, become crypto tokens that trade around the clock. Take Ondo Finance and Securitize, for instance.

They’ve been busy little bees, helping issue short-dated Treasury tokens last year. While projects like BlackRock’s BUIDL let investors own U.S. debt on Ethereum with transparency.

But wait, there’s more. Other RWAs are jumping on this bandwagon faster than kids chasing an ice cream truck, making the TradFi vs DeFi convo more interesting.

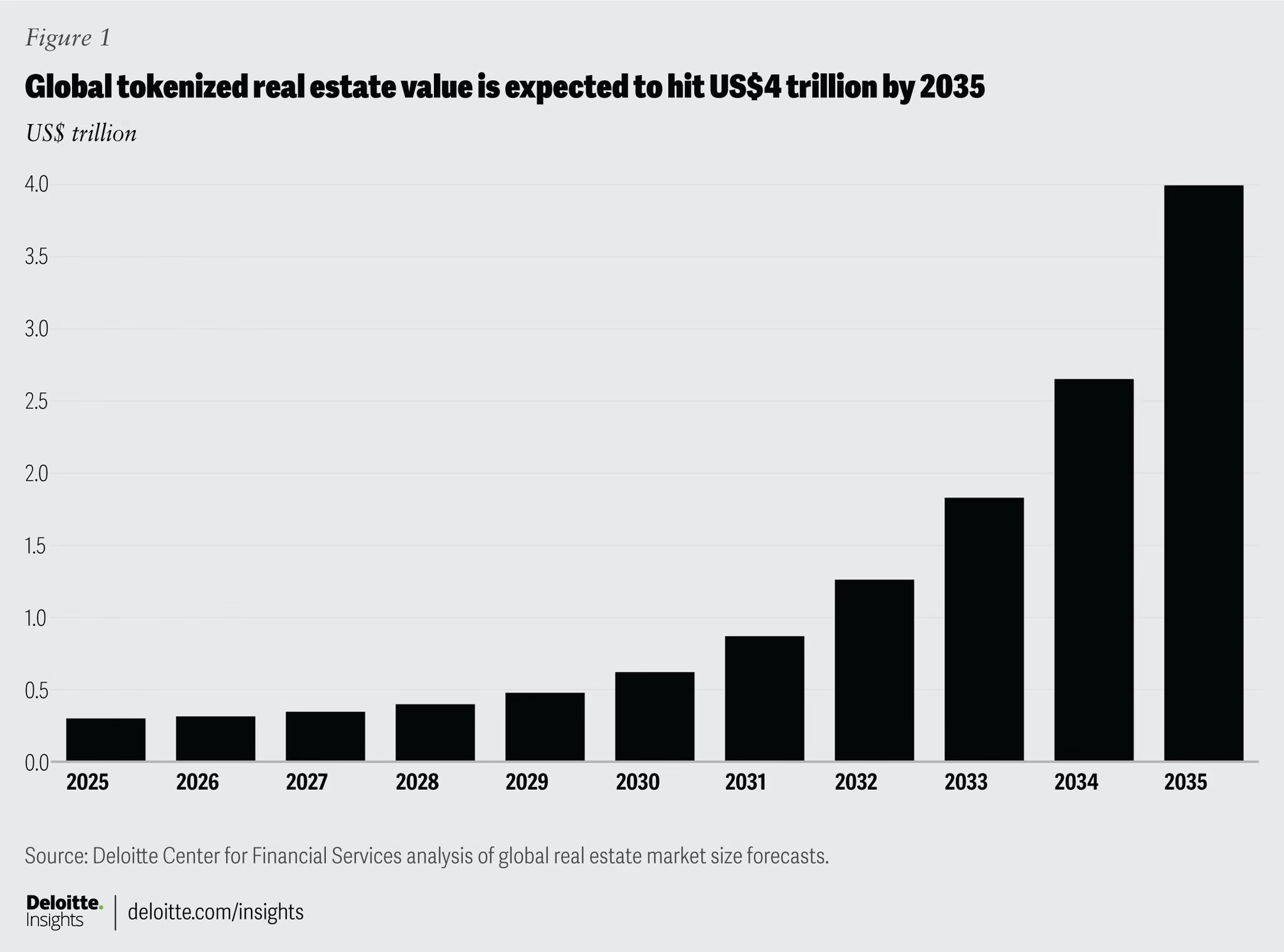

Kin Capital is cooking up a $100 million tokenized real-estate debt fund on the Chintai blockchain, while groups in Canada and India have launched blockchain-backed property developments worth hundreds of millions. According to Deloitte:

“Real estate asset tokenization can allow institutional investors to create custom portfolios with tokens that match their investment thesis.”

The rise of RWAs is blurring the lines between Wall Street and Web3. They are no longer sworn enemies. Banks get to streamline their creaky old systems while DeFi platforms gain by unlocking massive pools of high-grade collateral. It’s a match made in… well, maybe not heaven, but definitely in a very profitable industry.

“Every stock, every bond will have its own basic CUSIP; it will be on one general ledger; every investor, you and I, will have our own number, our own identification”— Larry Fink, CEO of BlackRock

Moreover, JPMorgan’s Kinexys unit has been showing off, demonstrating delivery-versus-payment between a private bank ledger and a public blockchain. They’re using Chainlink’s cross-chain tools to settle tokenized Treasury swaps with precision. We probably haven’t seen an end to this TradFi vs DeFi feud.

“By securely and thoughtfully connecting our institutional payments solution with both external public and private blockchain infrastructures seamlessly, we can offer our clients and the broader financial ecosystem a wider range of benefits and scalable solutions for settling transactions,” — Nelli Zaltsman, head of platform settlement solutions at Kinexys.

On the flip side, DeFi protocols (like Ondo or lending markets) gain new collateral and fixed income pools as tokenized bonds flow in. Oracles like Chainlink and Pyth are feeding live Treasury rate data on-chain, enabling DeFi lenders to price loans against official benchmarks. Maybe we’re gradually moving from TradFi vs DeFi to TradFi and DeFi; something like a ‘cohabitation’.

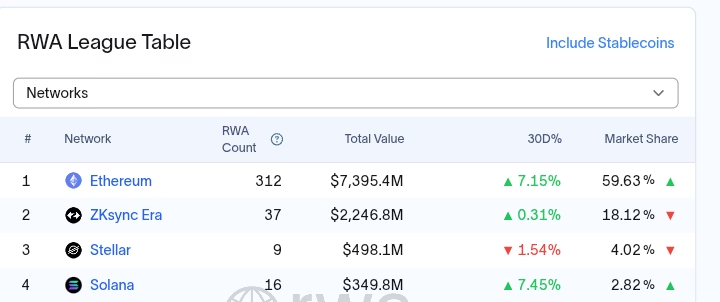

Ethereum doesn’t just dominate RWA tokenization, it owns the damn construction site. With its battle-tested smart-contract framework and a DeFi ecosystem that’s heavier than Dubai’s Business Bay traffic, it’s become the go-to foundation for anyone serious about putting real-world assets on-chain.

As seen in RWA.xyz, of the more than $20 billion in tokenized assets, Ethereum commands approximately 60% of the market share. This is more reason why ‘TradFi and DeFi’ seems to now make better sense than TradFi vs DeFi.

Here’s the thing that’ll make you sit up: Stablecoins (e.g., USDC, USDT), the bedrock of on-chain finance, run almost entirely on Ethereum, underpinning protocols for tokenized U.S.

Treasuries, commodities, and more. The institutional money isn’t just watching. They’re diving in. BlackRock’s BUIDL fund was built on Ethereum and quickly reached over $2.8 billion. So, when the world’s biggest asset manager picks your blockchain, you know you’re doing something right.

Now flip the script. While Ethereum’s busy being the wise elder, Solana’s the young hotshot revving a sports car in the parking lot. Solana offers blazing throughput and low fees, which many see as ideal for high-volume RWA flows.

Its parallelized architecture can handle on the order of +60,000 TPS at a low cost, letting applications tokenize billions in bonds or real estate without the network breaking a sweat.

This isn’t just tech flexing because it has attracted some serious players. R3, an enterprise blockchain firm backed by 500+ banks (including HSBC, Bank of America, and MAS), chose Solana for its $10 billion asset pipeline, building a permissioned consensus layer so banks can tap DeFi liquidity on a public chain.

But wait, there’s more to talk about the TradFi vs DeFi conversation. DeFi projects are deploying RWA tools on Solana: Centrifuge is issuing a $400 million short-dated Treasuries fund (deJTRSY) on Solana’s chain, so Solana users can earn yields on T-bills via Raydium or Kamino.

Before you start throwing money at everything that moves, let’s talk about the elephants in the room. Tokenized RWAs have regulators and auditors watching closer than a hawk eyeing a mouse. Jurisdictions worldwide are wrestling with whether on-chain asset tokens count as securities.

One day you’re innovating, the next day you’re getting a harsh letter from someone with three letters after their name: the SEC.

Then there’s the oracle problem. Oracles that feed real-world data on-chain represent a technical risk that could make your head spin. If price feeds or proof-of-reserves fail, a tokenized asset could be mispriced or under-collateralized.

Thankfully, some smart folks saw this coming. Projects like Chainlink mitigate this with decentralized oracle networks and PoR services, i.e, Chainlink’s feeds våerify that on-chain tokens are fully backed and use multiple data sources to resist manipulation.

Several crypto-native firms are racing to fill the RWA niche. Ondo Finance offers tokenized Treasury funds. As of January 28, 2025, its OUSG short-term fund (backed by BlackRock’s BUIDL asset) had about ~4.2% APY and holds ~$184 million in assets. Ondo even plans to deploy OUSG on Ripple’s XRP Ledger, broadening access to institutional bonds.

Then there’s Maple Finance, the VIP lounge of DeFi lending, which runs permissioned lending pools for institutions. Its USDC cash-management pool lets accredited investors park stablecoins in 1-month T-bills, all underwritten by real-world credit checks. And there’s also Securitize, a compliance-focused platform that powers many enterprise token issuances.

It acts as a transfer agent and placement agent for funds like BlackRock’s BUIDL and an Apollo credit fund, ensuring tokens meet securities laws. By mid-2025, Securitize claims billions of dollars tokenized under its roof.

When you get to have this thought “Tokenized U.S. Treasuries now yield 5% on-chain—are banks or DeFi protocols the real winners?”, Remember that it’s an unfolding saga, neither side holds the position. Banks wield the pen of regulation and huge funds, while DeFi pens the code of innovation and round-the-clock markets. Together they author a new chapter in finance.

For now, let’s keep watching the birth of a new financial hybrid, part Wall Street efficiency, part crypto innovation. And whether banks or DeFi protocols come out on top might be the wrong question entirely. Maybe they’re both winning, and we’re just witnessing the most profitable dance-off in financial history. Stay tuned to The Bit Gazette for more updates as the TradFi vs DeFi battle rages on. Thank you.

Copyright © 2025 - The Bit Gazette.

{kind=link}