- Trending

- Comments

- Latest

Yield-bearing stablecoins have become a flashpoint in Washington’s fast-moving crypto policy debate, after Bank of America CEO Brian Moynihan warned that trillions of dollars could flow out of the U.S. banking system if interest-paying digital dollars are allowed to scale.

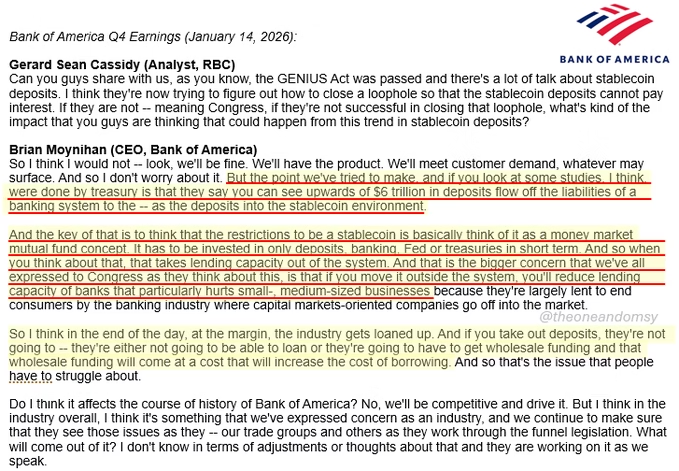

Speaking during Bank of America’s quarterly earnings call on Wednesday, Moynihan said as much as $6 trillion in deposits—roughly 30% to 35% of total U.S. commercial bank balances—could migrate into stablecoins under certain regulatory outcomes. The comments underscore rising concern among traditional lenders that yield-bearing stablecoins could fundamentally reshape how Americans store cash.

Moynihan said the estimate was grounded in Treasury Department studies and linked the potential shift directly to ongoing legislative discussions over whether stablecoin issuers should be allowed to offer yield.

At the heart of the debate is whether yield-bearing stablecoins should be permitted to offer returns similar to bank deposits or money market funds, without being subject to the same regulatory framework as insured banks.

According to Moynihan, many current stablecoin structures already resemble money market mutual funds more than traditional checking or savings accounts. Issuers typically hold reserves in short-term instruments such as U.S. Treasurys or cash equivalents, rather than recycling deposits into consumer and business loans.

“That money is not being lent back into the economy,” Moynihan told analysts. “If you take out deposits, banks are either not going to be able to loan or they’re going to have to turn to wholesale funding.”

He added that wholesale funding—such as borrowing from capital markets—tends to be more expensive and less stable, potentially raising borrowing costs across the economy if yield-bearing stablecoins siphon off deposits at scale.

The warning comes as lawmakers race to finalize a long-awaited crypto market structure bill. The Senate Banking Committee, chaired by Senator Tim Scott, released a revised draft on Jan. 9 that directly addresses the issue of interest and rewards on stablecoins.

The proposal would prohibit digital asset service providers from paying interest or yield simply for holding stablecoins, effectively curbing the spread of yield-bearing stablecoins in their most bank-like form. At the same time, the bill allows activity-based rewards tied to functions such as staking, liquidity provision, or posting collateral, drawing a line between passive balances and active participation.

That distinction is central to the current policy fight. Banking groups argue that paying yield on idle stablecoin balances would amount to deposit-taking without deposit insurance, capital requirements, or access to the Federal Reserve’s backstop.

Crypto firms, however, contend that yield-bearing stablecoins represent financial innovation rather than regulatory arbitrage. They argue that tokenized dollars backed by Treasurys offer transparency, efficiency, and real-time settlement that traditional banks struggle to match.

Coinbase CEO Brian Armstrong publicly withdrew support for the Senate bill on Wednesday, saying its current language would effectively eliminate stablecoin rewards and stifle competition. “We can’t support a framework that bans basic features users expect,” Armstrong wrote, referencing restrictions that would hit yield-bearing stablecoins.

That pushback highlights growing fractures within the crypto industry itself, as exchanges, issuers, and infrastructure providers jockey for favorable treatment in the final legislation.

From the banking sector’s perspective, the risk is systemic. Deposits form the backbone of bank lending, funding mortgages, small business loans, and consumer credit. A large-scale shift into yield-bearing stablecoins could shrink that base, forcing banks to curtail lending or raise rates.

Moynihan emphasized that his comments were not an indictment of blockchain technology itself, but a warning about unintended consequences if regulatory lines are blurred. “This is about how the system works,” he said. “If deposits move, lending capacity moves with them.”

Industry analysts note that the $6 trillion figure represents a worst-case scenario, assuming broad consumer adoption and permissive regulation. Still, even a fraction of that migration into yield-bearing stablecoins could have meaningful impacts on liquidity and credit availability.

The proposed legislation has also drawn criticism beyond deposit dynamics. A recent Galaxy Research report warned that the bill could significantly expand Treasury Department surveillance powers over digital asset transactions, raising privacy concerns for users and developers.

Meanwhile, political scrutiny has intensified following reports that President Donald Trump earned hundreds of millions of dollars from family-linked crypto ventures, prompting renewed debate over ethics provisions in the bill.

More than 70 amendments were filed ahead of the committee’s planned markup this week, reflecting intense lobbying from both banking associations and crypto firms with competing visions for yield-bearing stablecoins and their role in the financial system.

Late Wednesday, Senator Scott announced that the scheduled markup had been postponed, signaling that consensus remains elusive. “Everyone remains at the table working in good faith,” he said, as negotiations over stablecoins, surveillance, and market structure continue.

For now, yield-bearing stablecoins sit at the center of a high-stakes policy crossroads—one that could determine whether digital dollars complement the banking system or compete directly with it.

As Moynihan’s warning makes clear, the outcome will shape not just crypto markets, but the future flow of trillions of dollars across the U.S. financial system.

Copyright © 2025 - The Bit Gazette.

{kind=link}