- Trending

- Comments

- Latest

In crypto, words have specific technical meanings, until marketing departments get hold of them. The biggest casualty of this trend is the word “staking.”

Open almost any exchange app, and you’ll see a button that says “Stake your USDT for 8% APY.”

Here’s the problem: You cannot stake USDT. It is technically impossible.

What you’re actually doing is lending. While both earn you passive yield, the mechanics, and critically, the risks are completely different.

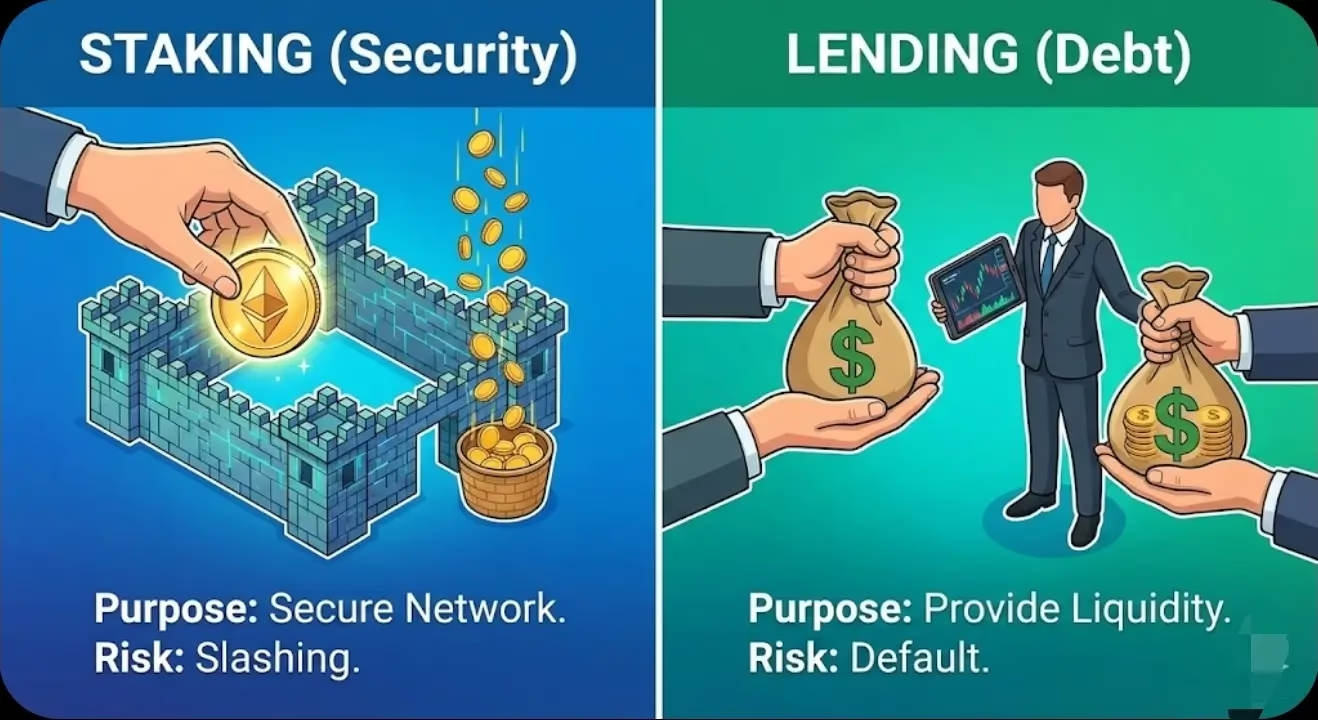

True staking is a technical contribution to the security of a blockchain.

How it works: You lock up a native asset (like Ethereum, Solana, or Cardano) to a validator node. This acts as a “security deposit” that helps the network approve transactions.

Where yield comes from: The network pays you newly created coins (protocol inflation) and transaction fees for securing the system.

The risk: Slashing. If your validator misbehaves or goes offline, the network can penalize your deposit, you lose a portion of your principal.

Key constraint: You can only stake Proof-of-Stake assets. You cannot stake Bitcoin (Proof-of-Work) or stablecoins (no blockchain to secure).

Example: When you stake ETH, you’re securing Ethereum’s network. If your validator approves fraudulent transactions, the protocol can slash 0.5-1 ETH (or more for serious violations). Current ETH staking APY: ~3-4%.

Lending is exactly what it sounds like: you’re acting as a bank.

How it works: You deposit assets (USDC, USDT, BTC) into a pool like Aave or give them to a platform like Kraken. They lend those funds to borrowers, usually traders seeking leverage.

Where yield comes from: Borrowers pay interest. That interest is passed to you.

The risk: Counterparty and credit risk. If borrowers default and liquidations fail, or if the platform gets hacked or goes insolvent, your money is gone.

Key feature: You can lend almost anything, including stablecoins and Bitcoin.

Example: When you deposit USDC into Aave, traders borrow it for leverage. If markets crash faster than the liquidation system can handle, you could face losses. Current Aave USDC APY: ~5-8%.

Staking = Security guard

Lending = Bank

Exchanges call everything “staking” because it sounds safer and more legitimate than “lending.”

“Lending” reminds users of credit risk and platform failures like Celsius and BlockFi, which collapsed in 2022 and wiped out billions in user funds, funds marketed as “staking” or “earn” programs.

By grouping all yield products under “Staking” or “Earn,” platforms simplify their interface but obscure fundamental risk differences.

| Feature | Staking | Lending |

|---|---|---|

| Purpose | Securing blockchain | Providing borrower liquidity |

| Yield Source | Protocol inflation + fees | Borrower interest payments |

| Assets | Only PoS coins (ETH, SOL) | Any asset (USDT, BTC, etc.) |

| Main Risk | Slashing penalties | Defaults, platform insolvency |

| Typical APY | 3-7% | 5-15% |

| Withdrawal | 1-21 days (unbonding) | Often instant or same-day |

Quick rule: Earning yield on USDT, USDC, or BTC? You’re lending.

Lending typically offers higher yields (5-15%) because it carries more risk. Staking yields are lower (3-7%) but more predictable.

With custodial platforms (exchange holds your keys), yes, if they go bankrupt like Celsius or FTX. With self-custodial staking/DeFi, you face technical risks (bugs, slashing) but not platform bankruptcy.

Neither is “safe.” Staking has protocol-level risks (slashing, usually <1% losses). Lending has counterparty risks (defaults, hacks, insolvency, potentially 100% loss).

Products like Lido’s stETH let you stake ETH while maintaining liquidity. You can then lend these tokens, combining both risk profiles.

When you click “Stake USDT” and earn 8%, you’re lending to borrowers and taking on credit risk.

When you stake ETH to run a validator, you’re securing the network and risking slashing penalties.

Both are legitimate ways to earn passive income. Both carry risk. The problem is platforms using the same word for fundamentally different activities.

Understanding the difference is the first step to managing your risk appropriately.

Copyright © 2025 - The Bit Gazette.

{kind=link}