- Trending

- Comments

- Latest

On May 29, nearly $7.5 billion worth of Bitcoin and Ethereum options expired on Deribit, making it one of the largest monthly crypto derivatives events of 2026. Traders expected the usual “max pain” dynamics to emerge the tendency for price to drift toward levels where the largest number of options expire worthless.

But this expiry did not behave the way many expected.

Instead of recovering toward max pain, both Bitcoin and Ethereum remained trapped well below key strike levels. Bitcoin hovered around $73,350 while its estimated max pain level sat near $75,000. Ethereum struggled around $2,003 despite a max pain level near $2,200.

The failure to recover was the real signal.

Billions in bullish call options expired worthless, institutional selling pressure overwhelmed dealer hedging flows, and the market delivered a sharp reminder that derivatives alone cannot force a rally when broader liquidity conditions remain weak.

This was not a bullish pin.

It was a bearish trap.

The May 29 expiry represented roughly 35% of Deribit’s total open interest, reinforcing how dominant derivatives have become in crypto market structure.

Bitcoin accounted for more than $6.2 billion in notional exposure while Ethereum contributed another $1.3 billion. The positioning heading into expiry appeared modestly bullish, with put/call ratios below 1.0 for both assets a sign that traders were leaning toward upside recovery.

Instead, the opposite happened.

Bitcoin fell roughly 5% during the week leading into expiry, while Ethereum hovered dangerously close to the psychological $2,000 support level. By settlement, a large share of bullish call positioning at $80,000, $82,000, and $85,000 had become effectively worthless.

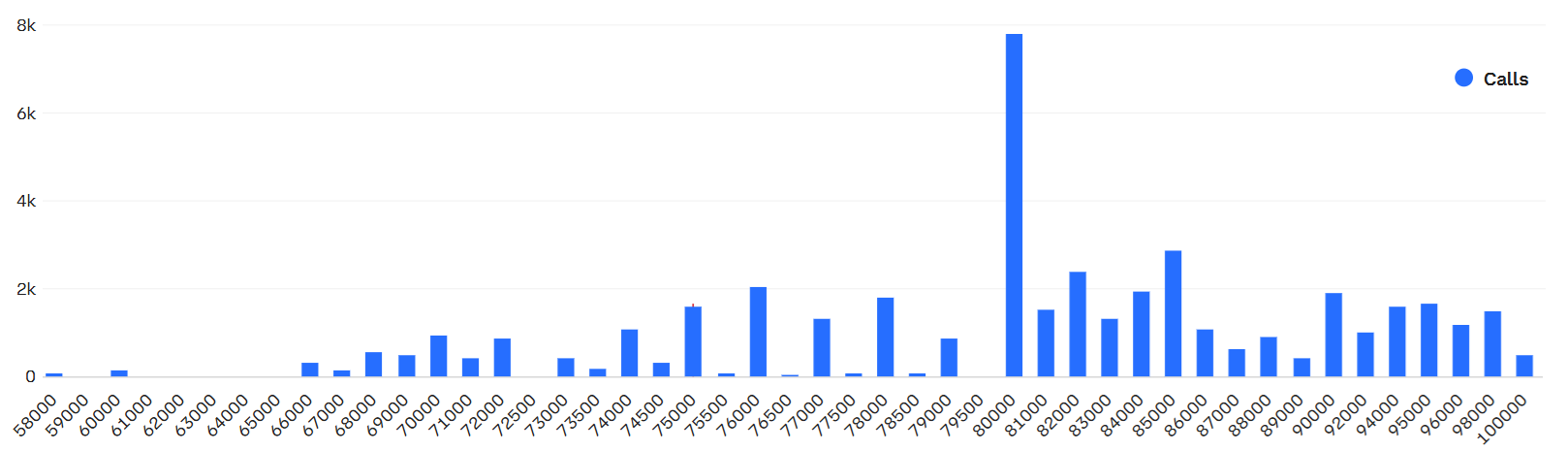

Friday Bitcoin call (buy) options open interest at Deribit, BTC. Source: Deribit

The market never came close to reaching those strikes.

That disconnect between positioning and outcome is what made the expiry so important.

The “max pain” theory assumes that dealer hedging and positioning flows tend to pull price toward heavily concentrated strike zones into settlement.

But max pain is not a law of markets.

It is a tendency one that can fail when larger forces dominate the tape.

In this case, institutional selling pressure proved stronger than the stabilizing effects of dealer hedging.

Bitcoin needed only a modest rally of around 2.2% to reach its $75,000 max pain level. Ethereum required a stronger recovery of nearly 10% to reach $2,200. Neither move materialized.

That failure revealed how weak upside momentum had become.

Rather than acting like a magnet, max pain became a ceiling the market could not reclaim.

The most important force suppressing the market was not options positioning itself, but institutional capital leaving the system.

Since May 14, crypto ETFs had reportedly seen roughly $2 billion in outflows. Those outflows weakened spot demand precisely when bullish positioning required stronger buying pressure to keep higher strikes alive.

That created a self-reinforcing bearish loop:

By expiry day, much of the market’s bullish structure had already collapsed.

The options market was no longer supporting price.

It was simply reflecting the weakness already visible in spot flows.

The most painful part of the expiry was concentrated above the market.

More than $1.7 billion in Bitcoin call open interest sat around the $80,000 strike alone, with additional positioning clustered near $82,000 and $85,000.

Those levels never came under serious threat.

As Bitcoin remained near $73,000, most upside positioning expired out of the money. Traders who expected a late-stage recovery into expiry were effectively trapped.

This is where the idea of a “max pain trap” becomes important.

Many traders assumed the market would naturally drift upward because max pain sat above spot price. But the existence of a max pain level does not guarantee that dealers or institutions will force price toward it.

If broader flows remain bearish, the market can simply fail to recover.

That is exactly what happened on May 29.

The most important takeaway from the expiry is not simply that bulls lost money.

It is that crypto market structure itself has changed.

Short-term price action is increasingly driven by derivatives positioning, ETF flows, dealer hedging, and volatility exposure rather than organic spot demand. Price discovery now happens inside financial wrappers around Bitcoin as much as within Bitcoin itself.

That shift changes how traders should interpret market moves.

In earlier crypto cycles, retail momentum and spot accumulation often dominated short-term direction. In 2026, large expiries, ETF flows, and gamma positioning have become central forces shaping price behavior.

The May 29 expiry exposed that reality clearly.

Despite billions in open interest and a heavily watched max pain level above spot, the market could not generate enough real buying pressure to reclaim key strikes.

The derivatives structure pointed upward.

The underlying liquidity environment pointed downward.

Liquidity won.

The May 29 expiry reinforced several important lessons for market participants.

First, max pain should be treated as a reference point, not a guaranteed destination. Markets can ignore max pain entirely when larger macro or institutional forces dominate.

Second, ETF flows now matter as much as options positioning. A heavily bullish derivatives structure means little if spot liquidity continues deteriorating underneath it.

Third, weak implied volatility during a selloff can signal complacency rather than panic. In this case, volatility never exploded higher despite worsening price action, limiting the conditions needed for a fear-driven short squeeze.

Most importantly, traders should recognize that modern crypto markets are increasingly reflexive. Options positioning influences spot price, while spot weakness reshapes options positioning in return.

That feedback loop is becoming one of the defining mechanics of crypto trading in 2026.

The original expectation surrounding the expiry was straightforward: a massive options settlement would likely pin price upward toward max pain before triggering a post-expiry recovery.

But the real story turned out to be the opposite.

Bitcoin never reclaimed $75,000. Ethereum never recovered toward $2,200. Billions in calls expired worthless, and institutional selling pressure overwhelmed the stabilizing effect of dealer hedging.

Copyright © 2025 - The Bit Gazette.

{kind=link}