- Trending

- Comments

- Latest

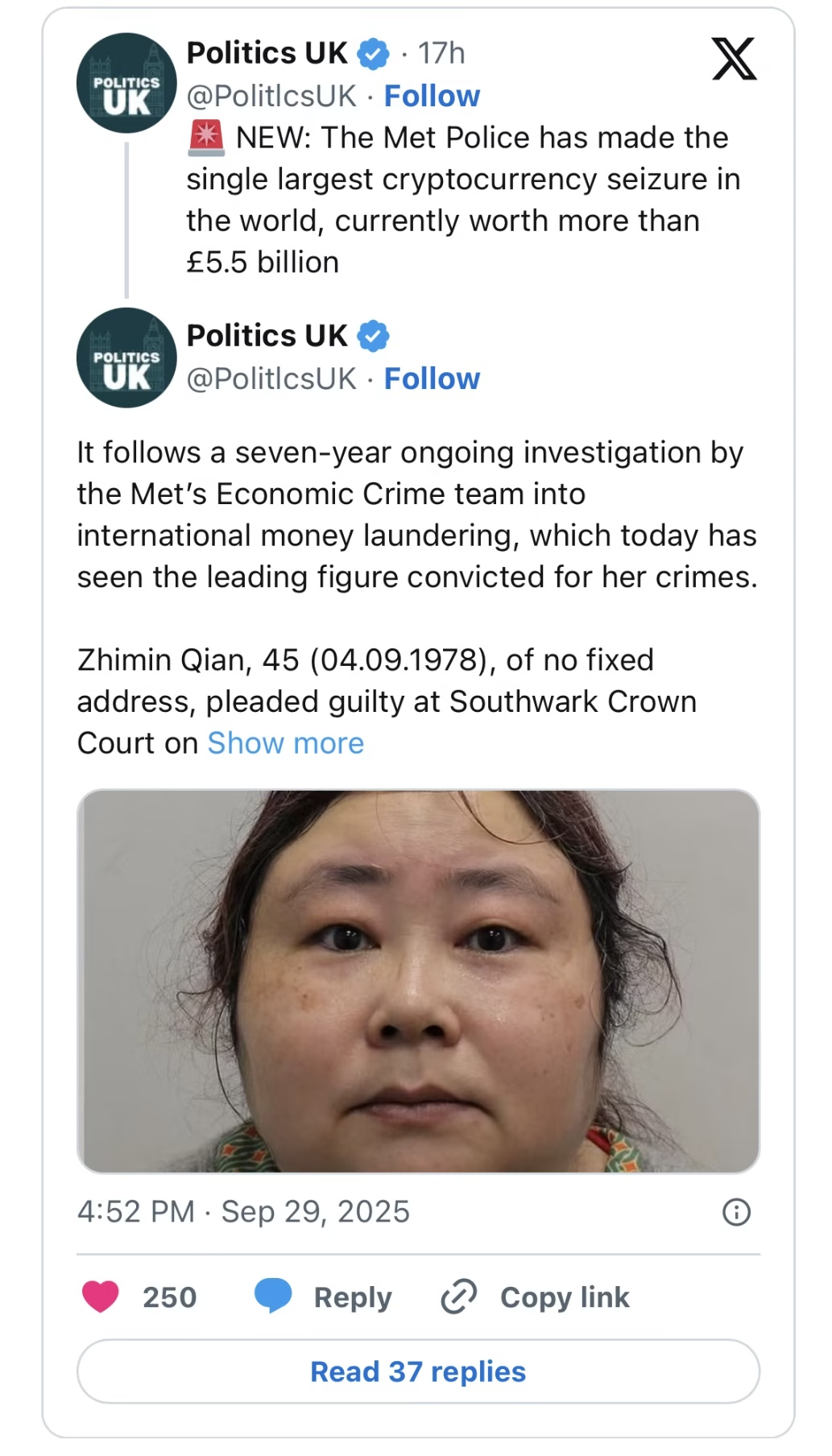

A London court has convicted Zhimin Qian, widely known as Yadi Zhang, for her role in a large-scale crypto investment scam that defrauded more than 128,000 victims in China between 2014 and 2017. The scheme, one of the biggest of its kind, funneled stolen funds into Bitcoin (BTC), eventually leading UK authorities to seize 61,000 BTC worth billions of dollars today.

The Metropolitan Police launched its probe in 2018 following reports of suspicious digital asset transfers. Investigators later discovered that Qian, operating under a false identity in Britain, had moved illicit funds into Bitcoin and attempted to launder them through luxury property purchases.

This was a painstaking, multi-jurisdictional investigation spanning seven years, said Detective Sergeant Isabella Grotto, who led the case. Qian’s arrest and conviction mark a major breakthrough in targeting the illicit use of crypto assets.

The 61,000 BTC seized is among the largest cryptocurrency confiscations in UK history. Authorities said Qian’s assets were directly linked to her large-scale crypto investment scam, which promised victims high daily dividends and life-changing returns.

Court documents reveal that Qian projected her company as a fintech innovator aligned with Beijing’s ambition to become a global leader in digital finance. In reality, it was a front for a large-scale crypto investment scam that exploited retail investors, retirees, and professionals across China.

Victims were persuaded by friends, family, or aggressive marketing to invest in a fund that claimed to generate consistent returns. Instead, prosecutors say, funds were siphoned off and converted into Bitcoin.

Crypto analyst Tom Robinson, co-founder of blockchain forensics firm Elliptic, noted that the case highlights how fraudsters exploit the early hype cycle of digital assets. This was a textbook example of a large-scale crypto investment scam, promising outsized gains in a market many did not fully understand, Robinson said.

Qian was not working alone. Her associate, Jian Wen, a 44-year-old former restaurant worker, was convicted in 2024 of laundering hundreds of millions in stolen Bitcoin. Wen went from modest living above a takeaway shop to occupying a luxury North London residence, acquiring two Dubai properties worth over £500,000.

According to prosecutors, Wen played a critical role in moving illicit funds into real estate and international accounts, further complicating efforts to trace the money.

The Qian conviction coincides with alarming data on physical crimes tied to digital assets. Security researcher Jameson Lopp, co-founder of CASA, reported a 169% surge in physical attacks on crypto holders globally over the past six months.

Since February, 35 violent incidents including kidnappings and armed robberies have been documented, with France alone accounting for 14 cases in 2025. One of the most disturbing occurred on September 6 in Cambridge, Canada, where a young man was abducted and forced at gunpoint to transfer crypto into a wallet.

“This rise in attacks shows that criminals view crypto as both a digital and physical target,” Lopp said. “The Qian case may be about a large-scale crypto investment scam, but it underscores the broader risks investors face when holding or moving digital assets.”

Qian is currently in custody and awaiting sentencing at Southwark Crown Court. UK authorities have not yet disclosed how seized assets might be returned to Chinese victims of the large-scale crypto investment scam, though international cooperation is expected.

For regulators, the case highlights the urgent need for cross-border coordination. With cryptocurrencies moving seamlessly across jurisdictions, scams like Qian’s exploit gaps in enforcement.

Legal experts argue that frameworks such as the EU’s Markets in Crypto-Assets Regulation (MiCA) and Singapore’s digital payments framework could serve as models. However, global adoption of consistent rules remains limited.

“Cases like this illustrate why global regulators must act quickly,” said Caroline Malcolm, Head of Public Policy at Chainalysis. “Without harmonized oversight, another large-scale crypto investment scam could easily emerge and impact investors worldwide.”

Copyright © 2025 - The Bit Gazette.

{kind=link}