- Trending

- Comments

- Latest

A new initiative testing tokenized sterling deposits has been launched by UK Finance, the trade association representing more than 300 financial services firms across the United Kingdom. The pilot project, announced Friday, aims to create a digital representation of traditional British pound commercial bank money and could reshape payments, settlement, and fraud prevention across the financial system.

The trial will run until mid-2026, with backing from six major banks — Barclays, HSBC, Lloyds Banking Group, NatWest, Nationwide, and Santander UK.

The tokenized sterling deposits pilot aims to test how tokenization can provide faster payments, reduced fraud risks, and more efficient settlement. Unlike cryptocurrencies or stablecoins, tokenized deposits are backed by commercial bank money and remain under existing banking regulation.

“Tokenized deposits are not about replacing money; they are about enhancing its functionality in a digital economy,” — Charlotte Smith, Head of Payments Policy at UK Finance, in a statement to The Financial Times.

The project is seen as a crucial step for the UK in preparing its financial infrastructure for the digital era. By exploring programmable money, banks and regulators hope to improve efficiency for both retail and wholesale financial activities.

Quant Network, a UK-headquartered blockchain interoperability provider, will supply the infrastructure for the tokenized sterling deposits pilot. The company previously played a central role in the first phase of the Regulated Liability Network (RLN), launched in 2024 to test shared ledger-based financial market systems.

Quant’s founder and CEO, Gilbert Verdian, emphasized that the project extends beyond payments:

“This initiative is about enabling new forms of programmable money that will fundamentally transform how value is moved and managed,” — Gilbert Verdian, CEO, Quant Network.

The involvement of the same six banks from the RLN project underscores continuity in the UK’s approach to exploring tokenization within existing regulatory and banking frameworks.

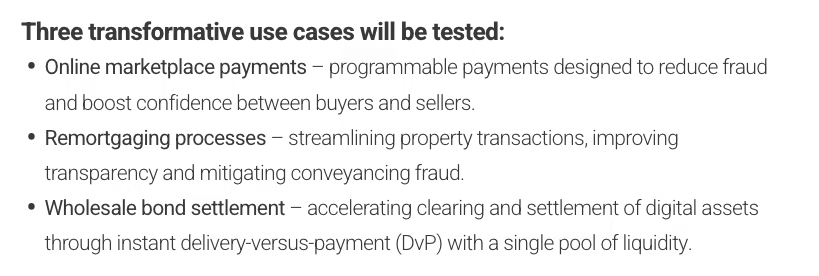

During the pilot, the tokenized sterling deposits project will test three core applications:

These test cases reflect the Bank of England’s broader interest in digital settlement models and align with global financial experiments in tokenization.

“Tokenization has the potential to cut costs and improve trust across the value chain,” — Michael Green, Senior Economist, Bank of England, in remarks at a recent policy forum.

The rollout of tokenized sterling deposits comes as the UK prepares for a new crypto regulatory regime. The Financial Conduct Authority (FCA) is finalizing its framework for crypto-assets, expected to take full effect in 2026.

In April 2025, the UK Treasury published its policy note on the “Future financial services regulatory regime for crypto assets,” drawing a clear distinction between stablecoins, tokenized deposits, and electronic money.

Meanwhile, the European Union has advanced its Markets in Crypto-Assets (MiCA) regulation, which took effect in late 2024. However, MiCA does not cover tokenized deposits, leaving them governed by traditional banking rules. This divergence highlights the UK’s attempt to position itself as a leader in regulated tokenization.

The tokenized sterling deposits pilot is set to continue until mid-2026, with findings expected to inform broader financial sector reforms and potential deployment of commercial tokenized money.

For policymakers, the results could shape how the UK approaches digital pounds, complementing the Bank of England’s separate work on a retail central bank digital currency (CBDC).

For investors and financial institutions, the project signals growing momentum behind tokenization which is a development that could eventually affect how mortgages, bonds, and even everyday transactions are processed.

“Programmable money represents the next stage of financial evolution. With tokenized deposits, banks can deliver efficiency without undermining stability,” — Elaine Parker, Research Director, DeFi Watch UK.

As the pilot unfolds, all eyes will be on whether the UK can balance innovation with regulatory oversight, ensuring tokenization strengthens rather than destabilizes the financial system.

Copyright © 2025 - The Bit Gazette.

{kind=link}