- Trending

- Comments

- Latest

The U.S. Internal Revenue Service (IRS) has secured a crypto tax fraud conviction, marking a critical milestone in the regulation of digital assets. Frank Richard Ahlgren III was sentenced to two years in federal prison and fined $1.1 million for evading taxes on cryptocurrency sales.

This conviction not only sets a legal precedent for crypto-related tax fraud but also signals that tax authorities worldwide are taking aggressive steps to ensure compliance in the burgeoning crypto economy.

According to a January 27 blog post by blockchain analytics firm Chainalysis, this is the first time the IRS has successfully prosecuted tax fraud that exclusively involved cryptocurrency.

Chainalysis emphasized the global implications of the case, calling it a “significant win for the Department of Justice and justice ministries worldwide.”

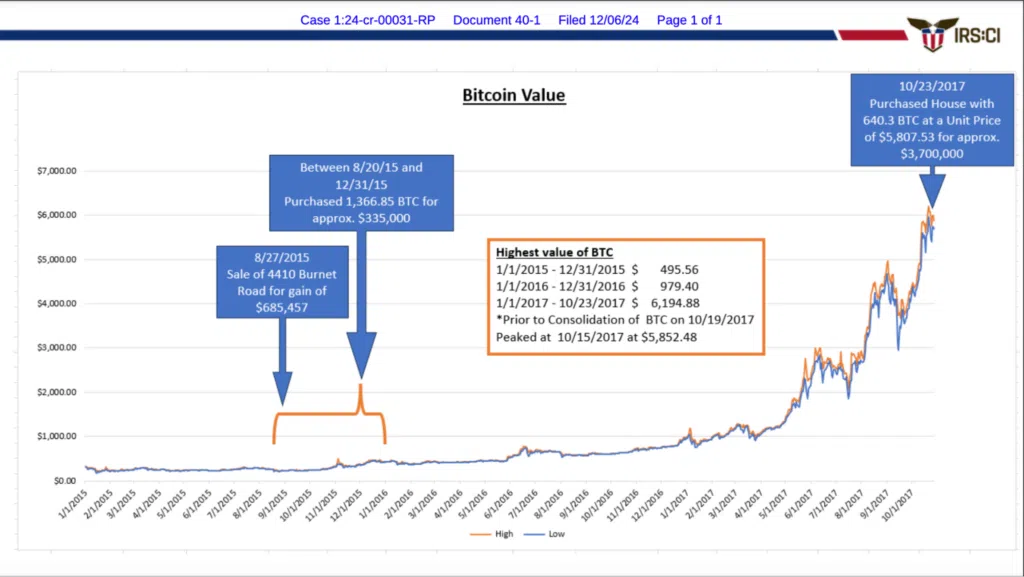

The case against Ahlgren began unraveling when he purchased a $4 million mansion in Park City, Utah, using profits from Bitcoin sales. Investigators revealed that Ahlgren employed complex tactics to conceal his earnings, including the use of CoinJoin mixers, Wasabi Wallet, peer-to-peer trading platforms, and structured cash deposits. These methods, often touted as privacy-enhancing tools, were ultimately insufficient to evade the scrutiny of blockchain analytics.

“Although Ahlgren thwarted the authorities for a time from performing some calculations, his conviction and sentencing illustrate how on-chain tax evasion is traceable and has real-world consequences,” stated Chainalysis.

Ahlgren’s crypto tax fraud conviction stemmed from transactions dating back to 2015. That year, he purchased 1,366 BTC for approximately $676,170, which later surged in value as Bitcoin prices skyrocketed. Despite amassing significant wealth, Ahlgren falsified his tax filings to underreport the value of his cryptocurrency holdings.

Blockchain investigators tracked his transactions across multiple wallets and exchanges, ultimately exposing the elaborate scheme. Tools like CoinJoin and Wasabi Wallet, designed to obscure transaction details, proved ineffective against advanced blockchain forensics employed by agencies like the IRS.

This case underscores the growing sophistication of regulatory bodies in monitoring blockchain activity. For crypto traders attempting to evade taxes, it’s a stark reminder that the pseudonymous nature of blockchain does not equate to complete anonymity.

The crypto tax fraud conviction is expected to have far-reaching consequences for the digital asset industry. With this case, the IRS has demonstrated its ability to navigate the complexities of blockchain technology, setting a precedent for future enforcement actions.

“This ruling sends a strong message that tax evasion in the crypto space will not be tolerated. It’s a wake-up call for investors and traders who think they can operate outside the law,” said Sheila Warren, CEO of the Crypto Council for Innovation, in an interview with Crypto News Today.

Beyond the IRS, other regulatory agencies and governments are likely to draw inspiration from this case as they ramp up efforts to combat tax fraud involving digital assets. The decision also reinforces the importance of compliance tools for crypto users, such as proper record-keeping and timely reporting of taxable events.

As the IRS celebrates its victory, legislative efforts surrounding crypto taxation continue to heat up. Senator Ted Cruz of Texas, alongside Senators Cynthia Lummis, Bill Hagerty, and Tim Sheehy, has vowed to challenge new IRS rules requiring decentralized crypto exchanges to collect customer information. These regulations, finalized in late 2024, mandate the collection of user data such as names and addresses, as well as the issuance of tax forms.

Cruz and his colleagues are leveraging the Congressional Review Act (CRA) to repeal what they have dubbed the “midnight rules” of the Biden administration. The CRA allows resolutions to bypass Senate filibusters, needing only a simple majority vote in both chambers. Congress has until mid-May to act on these regulations.

The crypto tax fraud conviction of Frank Ahlgren III highlights the increasing sophistication of tax authorities in tracking illicit activity in the digital asset space. As blockchain forensics tools continue to evolve, individuals attempting to exploit the perceived anonymity of cryptocurrency are likely to face greater challenges.

“The notion that blockchain transactions are anonymous is a myth,” remarked Michael Gronager, CEO of Chainalysis, in a statement. “This case proves that with the right tools and determination, illicit activities can and will be uncovered.”

For the crypto community, this conviction is both a cautionary tale and a call to action. Industry participants must prioritize transparency and compliance to avoid similar legal repercussions.

The IRS’s first crypto tax fraud conviction is a groundbreaking development in the regulation of digital assets. By securing a conviction against Frank Ahlgren III, the agency has sent a clear message to the global crypto community: tax evasion will not go unpunished.

As regulatory scrutiny intensifies, it is imperative for crypto investors and traders to ensure full compliance with tax laws. The conviction serves as a reminder that blockchain technology, while innovative, does not shield individuals from the reach of the law.

For the first time in history, a crypto tax fraud conviction has been secured by the IRS, marking a turning point in crypto-related financial crime enforcement. The landmark case not only underscores the IRS’s increasing vigilance but also serves as a warning to cryptocurrency traders evading taxes.

On December 2024, Frank Richard Ahlgren III was sentenced to two years in federal prison and fined $1.1 million for evading taxes on his Bitcoin sales. This crypto tax fraud conviction highlights the power of blockchain analytics tools in tracking illicit activity, even when sophisticated methods are used to obscure transactions.

For lawmakers, tax authorities, and industry leaders, this case marks the beginning of a new era in crypto enforcement—one where transparency, accountability, and compliance are non-negotiable. Get more from The Bit Gazette

Copyright © 2025 - The Bit Gazette.

{kind=link}