- Trending

- Comments

- Latest

The Financial Action Task Force released a report warning that peer-to-peer stablecoin transfers conducted through self-custody wallets present growing risks for sanctions evasion and money laundering.

The FATF identified the absence of regulated intermediaries in direct wallet-to-wallet transfers as a compliance blind spot that jurisdictions must address as stablecoin adoption expands.

According to the report, transfers executed directly between self-custody wallets can occur without the involvement of regulated intermediaries such as exchanges, custodians, or other virtual asset service providers (VASPs). That absence creates potential blind spots in Anti-Money Laundering (AML) supervision.

“Transactions conducted through unhosted wallets may fall outside the perimeter of regulated entities responsible for monitoring and reporting suspicious activity,” the FATF stated in its findings.

The concern driving FATF stablecoin regulation discussions is not that blockchain transactions are invisible—far from it. Public blockchain activity is permanently recorded and traceable onchain. However, the pseudonymous design of wallet addresses complicates real-world attribution, particularly when no regulated gateway is involved.

In effect, FATF stablecoin regulation efforts are focused on bridging the compliance gap that emerges when digital dollars move entirely outside supervised platforms.

Stablecoins have rapidly evolved from crypto trading tools into widely used payment instruments. They are increasingly employed for remittances, cross-border settlements, and online commerce, particularly in regions facing currency volatility.

As their utility grows, so does regulatory scrutiny.

The FATF stablecoin regulation report emphasizes that jurisdictions must evaluate the risks created by stablecoin arrangements and implement “proportionate” safeguards. These may include enhanced monitoring requirements when self-custody wallets interact with regulated exchanges, as well as clearer AML and counterterrorism financing obligations for entities involved in issuing and distributing stablecoins.

A compliance expert at a global financial advisory firm said the FATF stablecoin regulation guidance signals a maturation phase in digital asset oversight.

“Regulators understand that stablecoins are no longer peripheral,” the expert noted. “They’re integrated into payment flows. FATF stablecoin regulation is about ensuring compliance evolves at the same pace as adoption.”

The watchdog described P2P transfers via self-custody wallets as a “key vulnerability.” These transactions occur directly between users without a VASP or financial institution subject to reporting requirements.

That absence limits authorities’ ability to detect suspicious activity in real time.

Under FATF standards, regulated entities must conduct customer due diligence, maintain transaction records, and report suspicious transfers. When stablecoins move outside that ecosystem, FATF stablecoin regulation frameworks may struggle to apply effectively.

However, the watchdog also acknowledged an important nuance: blockchain transparency provides investigative value even in decentralized environments.

While attribution may be difficult, transactions remain traceable. Law enforcement agencies and analytics firms routinely use blockchain forensic tools to map flows and identify clusters of activity.

The FATF stablecoin regulation discussion, therefore, is less about anonymity and more about accountability triggers—specifically, when and how compliance obligations activate.

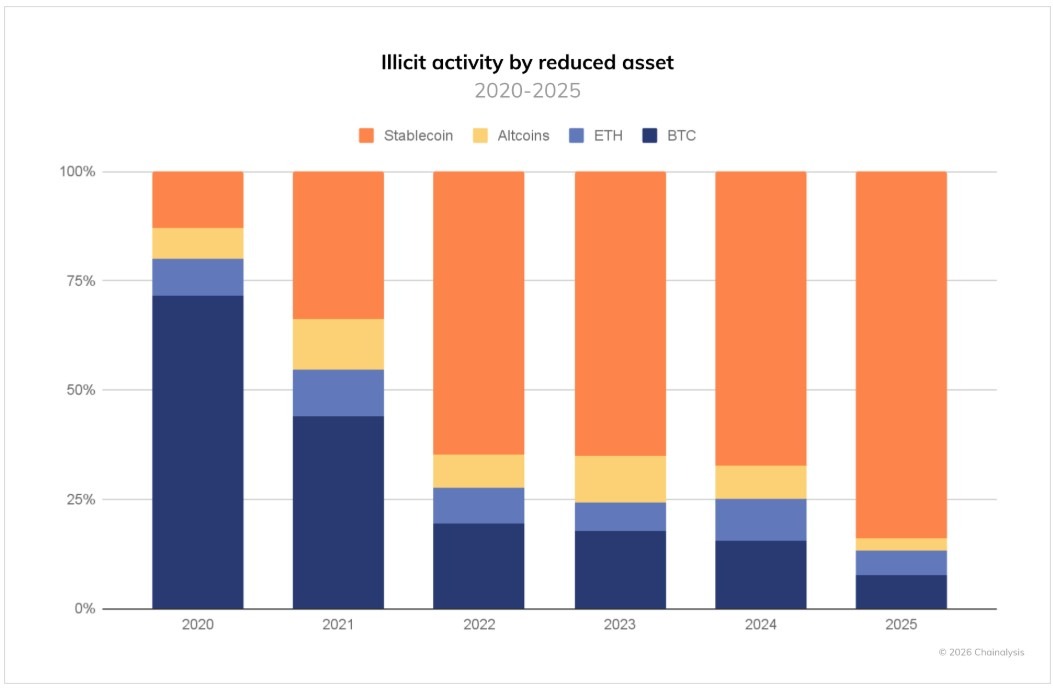

The report references findings from blockchain analytics firm Chainalysis, which estimated that illicit crypto addresses received at least $154 billion in 2025. Stablecoins accounted for 84% of illicit transaction volume during that period.

At first glance, the figure appears alarming. Yet Chainalysis emphasized an important contextual detail: illicit activity represented less than 1% of total crypto transaction volume.

FATF stablecoin regulation commentary reiterates this statistic, highlighting both the scale of absolute flows and the relatively small proportion of overall blockchain activity tied to crime.

A spokesperson from Chainalysis has previously noted, “While the absolute dollar value of illicit crypto activity can grow alongside broader adoption, the percentage share remains low compared to total transaction volume.”

For policymakers, FATF stablecoin regulation aims to prevent that percentage from rising as adoption accelerates.

The language used in the report repeatedly stresses “proportionate” safeguards—a term that signals a measured approach rather than blanket restrictions.

FATF stablecoin regulation recommendations do not call for prohibiting self-custody wallets. Instead, they encourage jurisdictions to conduct risk assessments and tailor mitigation strategies accordingly.

A policy analyst specializing in financial crime prevention said the tone of FATF stablecoin regulation guidance reflects a balancing act.

“On one hand, there’s recognition that stablecoins can enhance financial inclusion and payment efficiency,” the analyst said. “On the other, regulators want to avoid creating exploitable gaps. FATF stablecoin regulation is about calibrating that balance.”

One of the most sensitive aspects of the report relates to sanctions compliance. The watchdog warned that P2P stablecoin transfers conducted outside regulated environments may present opportunities for sanctions circumvention.

As geopolitical tensions persist globally, financial monitoring remains a priority for governments. FATF stablecoin regulation efforts are likely to influence how jurisdictions align digital asset rules with broader sanctions enforcement strategies.

Still, the report stops short of declaring stablecoins inherently high risk. Instead, it frames the issue as structural: where regulated oversight ends, vulnerabilities may begin.

As stablecoin adoption expands across payments and cross-border transfers, FATF stablecoin regulation guidance is expected to shape policy responses worldwide.

Jurisdictions will need to assess how self-custody wallet activity interacts with domestic AML frameworks. Exchanges and issuers may face clearer compliance expectations. Meanwhile, analytics tools and investigative techniques are likely to grow more sophisticated.

The overarching message is clear: stablecoins are now embedded in the financial system’s digital layer. Oversight mechanisms must adapt accordingly.

FATF stablecoin regulation does not signal a crackdown—it signals integration. The challenge for policymakers will be implementing safeguards that address real risks without stifling legitimate innovation.

For the crypto sector, the era of regulatory ambiguity around stablecoins is narrowing. FATF stablecoin regulation guidance makes one thing certain: as digital dollars circulate globally, compliance standards will follow closely behind.

Copyright © 2025 - The Bit Gazette.

{kind=link}