- Trending

- Comments

- Latest

Someone just destroyed $8.5 million worth of bitcoin, coins that had not moved since 2013, when the entire stash was worth less than $65,000. No one has claimed responsibility, and no one can explain why.

The unexpected Bitcoin burn immediately triggered intense speculation across the market, with analysts floating theories ranging from tax-loss harvesting and operational mistakes to illicit activity and even rogue artificial intelligence systems.

Blockchain researchers said the coins had remained untouched for more than 12 years before being permanently removed from circulation earlier this week.

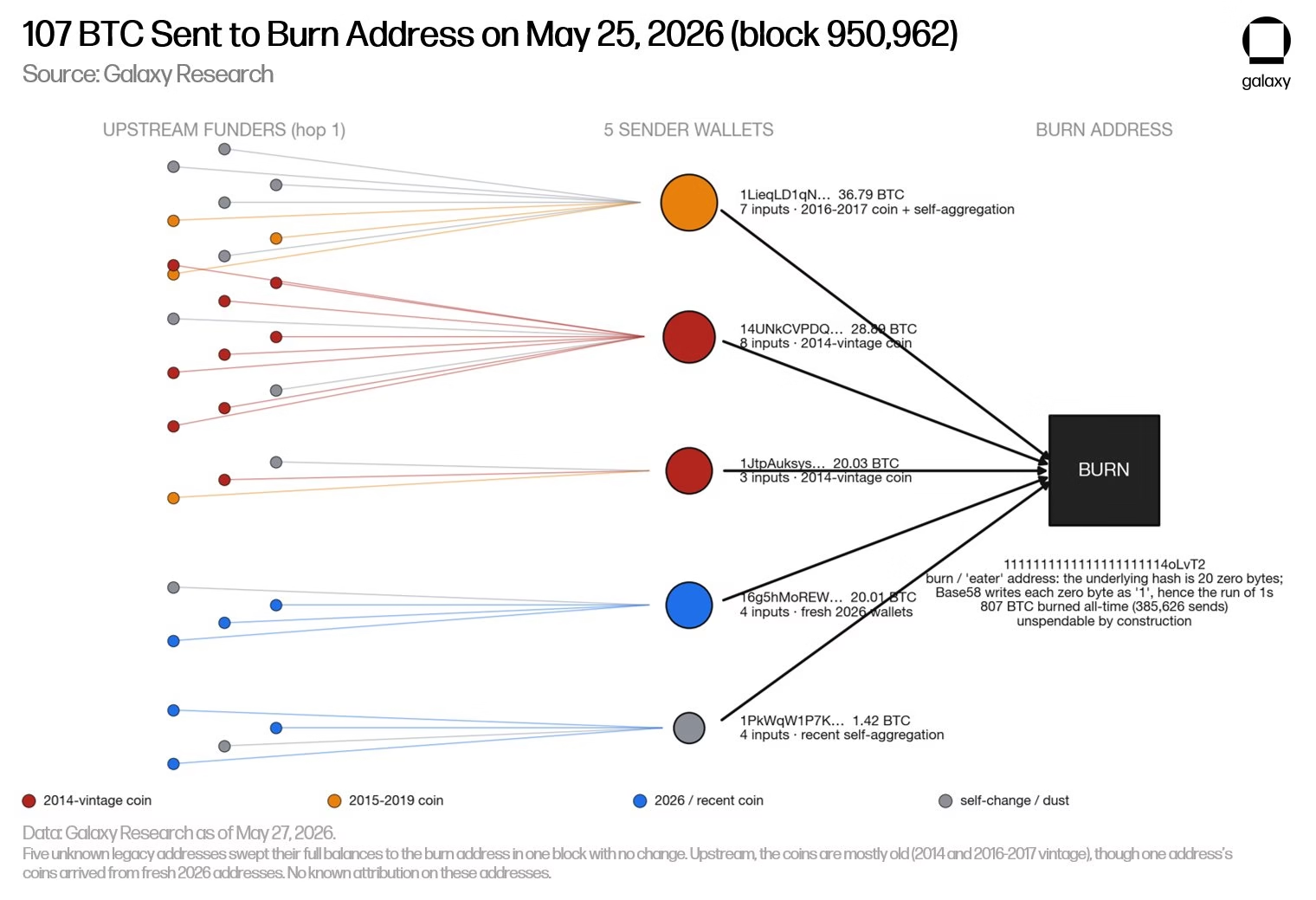

According to onchain data highlighted by Galaxy Research, five separate Bitcoin addresses transferred a combined 107 BTC into the well-known burn address beginning with “11111,” making the funds effectively inaccessible forever.

The unusual Bitcoin burn has now become one of the largest known BTC destruction events recorded in 2026.

The latest Bitcoin burn also pushed the total value stored inside the famous burn address to approximately 807 BTC.

Based on current market prices, that amount is worth nearly $59 million, according to blockchain intelligence platform Arkham.

Unlike some blockchain networks that include automated supply reduction mechanisms, Bitcoin does not possess a native burn function built into its protocol.

Instead, a Bitcoin burn occurs when users intentionally send BTC to wallet addresses that have no known private keys, making the coins permanently unrecoverable.

Although the tokens technically remain visible on the blockchain ledger, they can never be spent again. That process effectively removes the assets from active circulation forever.

The scale and timing of this particular Bitcoin burn surprised many observers because the destroyed coins were reportedly acquired around 2013, when Bitcoin traded below $600.

Since then, Bitcoin’s value has surged roughly 12,700%, according to market data from TradingView.

The decision behind this Bitcoin burn appears especially unusual because long-term holders are historically among the least likely participants to destroy valuable BTC holdings.

Most dormant wallets that reactivate after years of inactivity typically move funds to exchanges, institutional custodians, or updated storage systems rather than irreversible burn addresses.

That reality has intensified speculation surrounding the motive behind the Bitcoin burn.

Some analysts believe the transfer may have been intentional, while others suspect the event could have resulted from a catastrophic operational mistake.

The market reaction reflects how emotionally significant Bitcoin burns can become inside the crypto ecosystem.

Because Bitcoin has a permanently capped supply of 21 million coins, every large Bitcoin burn marginally increases scarcity by reducing the amount of BTC that can realistically circulate in the market.

Researchers and crypto executives quickly began offering competing explanations for the mysterious Bitcoin burn.

Galaxy Research suggested that the transfer may have been linked to tax-loss harvesting strategies or potentially connected to coins associated with illicit activity.

However, investigators reportedly found no direct evidence linking the funds to hacks, cybercrime operations, or known sanctions-related activity.

One of the more controversial theories surrounding the Bitcoin burn involved artificial intelligence.

Galaxy researchers floated the possibility that an AI agent handling wallet operations may have mistakenly transferred the funds to the wrong address.

That theory gained additional attention after Eric Balchunas, senior ETF analyst at Bloomberg, referenced the possibility of a “rogue AI agent” being responsible for the transfer.

Balchunas also mentioned other possibilities, including tax-related motives or even coercion scenarios involving kidnapping.

While such theories remain speculative, they demonstrate how unusual the Bitcoin burn appears even to experienced market observers.

Another explanation gaining traction points toward operational mistakes by centralized exchanges.

Conor Grogan, head of product business operations at Coinbase, said the Bitcoin burn was “most likely an exchange that messed up their cold storage transfers.”

That possibility has generated serious discussion because large exchanges frequently move dormant holdings between cold wallets and internal custody systems.

A simple configuration mistake involving address management could theoretically send funds into a burn address permanently.

Historically, crypto markets have witnessed several high-profile wallet mishaps involving incorrect addresses, lost private keys, and inaccessible storage devices. However, the sheer size of this Bitcoin burn makes the situation especially noteworthy.

Although the latest Bitcoin burn shocked markets, burn addresses themselves are not new within the broader crypto ecosystem.

Several blockchain projects have previously used proof-of-burn mechanisms to establish token distribution systems or validate network participation.

The specific “11111” address involved in this incident has appeared in earlier crypto experiments.

For example, the Bitcoin-based project Stacks used the same address during a 2015 proof-of-burn process tied to namespace registrations. Still, those historical burns were intentional protocol-level mechanisms.

The current Bitcoin burn stands apart because the destroyed funds carried an estimated value exceeding $8 million and originated from long-dormant holdings with no clear explanation.

The latest Bitcoin burn also feeds directly into one of Bitcoin’s strongest long-term narratives: scarcity.

Every permanently inaccessible coin further tightens available supply, especially as institutional demand for Bitcoin continues expanding globally.

Crypto analysts often estimate that millions of BTC may already be permanently lost due to forgotten private keys, destroyed hardware wallets, accidental transfers, and inaccessible early mining wallets.

This Bitcoin burn therefore adds to the growing portion of Bitcoin’s theoretical supply that may never re-enter circulation.

While 107 BTC represents only a small fraction of Bitcoin’s total supply, high-profile burns often attract significant attention because they visibly reinforce Bitcoin’s scarcity dynamics.

Beyond supply implications, the Bitcoin burn also serves as another reminder that crypto infrastructure still carries substantial operational risk.

Even after years of industry growth, blockchain systems remain unforgiving when errors occur.

Unlike traditional banking systems, crypto transactions are generally irreversible once confirmed on-chain.

If the latest Bitcoin burn resulted from a technical mistake or flawed automated process, the funds are likely unrecoverable forever.

That reality continues separating blockchain finance from traditional financial systems where transactions can often be reversed or disputed through intermediaries.

As institutional adoption grows, incidents like this may increase pressure on exchanges, custodians, and wallet providers to improve operational safeguards and transaction verification systems.

For now, the identity and motive behind the Bitcoin burn remain unknown.

No entity has publicly claimed responsibility for the transfer, and investigators have not released evidence identifying the wallet owner.

Theories surrounding taxes, AI systems, exchange mistakes, or illicit activity continue circulating across crypto communities, but none have been conclusively verified.

Until additional blockchain evidence emerges, the latest Bitcoin burn may remain one of the year’s most intriguing crypto mysteries.

What is already clear, however, is that more than $8.5 million worth of Bitcoin has now been removed from practical circulation permanently adding another chapter to the strange history of lost and destroyed digital wealth.

Copyright © 2025 - The Bit Gazette.

{kind=link}